The IMF and World Bank have agreed some positive changes to their system for monitoring debts of impoverished countries, though some large issues have been ignored. The system, known as the Debt Sustainability Framework, is important as it directly impacts on amounts of lending by the World Bank and other multilateral development banks, and influences lending decisions by governments and the private sector.

A key improvement is that some of the hidden cost from Public-Private Partnerships (PPPs) will now be included. This was one of the main demands of global civil society of the review, and 2,500 people wrote to the UK’s representative at the IMF asking for this change to be made. One of the main reasons government’s use expensive PPP schemes to provide public services is because they enable debts to be hidden. Hopefully the changes will bring PPPs onto more of a level playing field with other forms of public investment, though much more still needs to be done.

Another positive improvement, called for by global civil society, is to reduce the importance of World Bank assessments of economic policies in deciding how much debt impoverished countries can cope with. Under the old system, World Bank assessments of how widely free market economic policies have been introduced, including trade liberalisation, deregulation and regressive taxes, increased how much debt countries were thought to be able to take on, even though there is no evidence that these free market economic policies reduce the risk of debt crises. Following the review, these assessments will still be included, but they carry less importance.

The review acknowledges the importance of debts owed by the private sector in causing debt crises. However, changes to how the IMF’s and World Bank assessments work to ensure these are covered are being discussed by a follow-up process, happening between now and the end of 2017.

There are some other fundamental issues which have not been addressed. Some of these are not surprising. Global civil society called for debt assessments to be carried out by a body independent of creditors and debtors, rather than the World Bank and IMF, which are themselves significant lenders. It is not a shock to learn that the IMF and World Bank ignored this suggestion. However, the review does admit that judgement by the institutions has sometimes led to debt ratings being different.

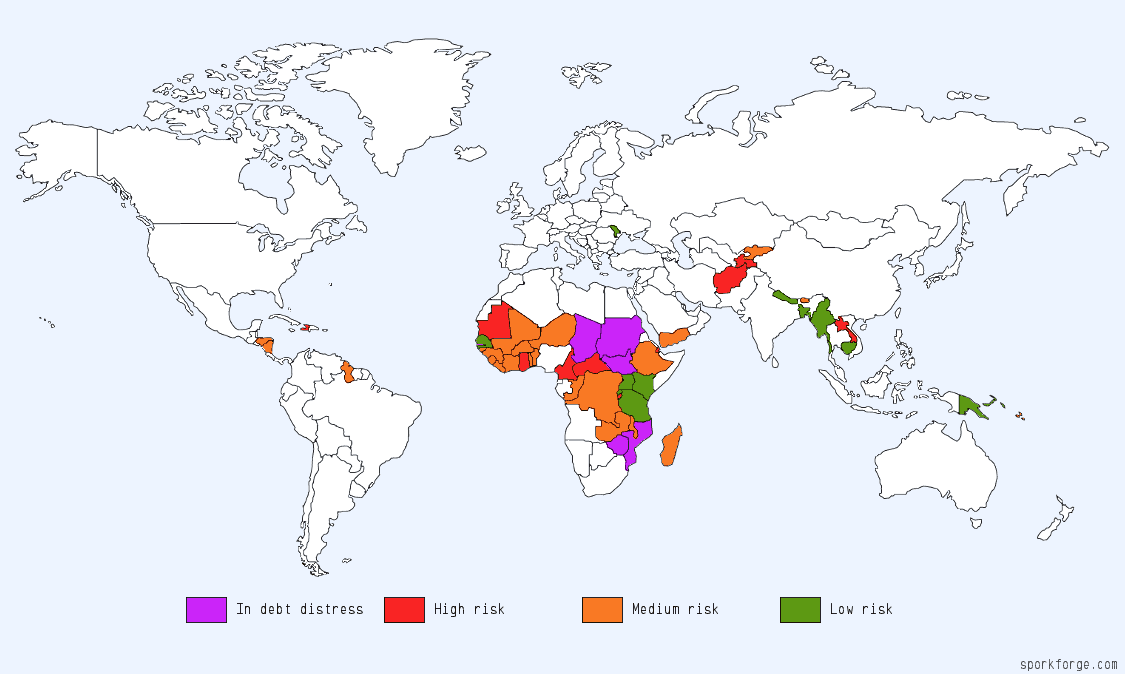

For example, in Mozambique, which is now in a large debt crisis, the review says that between 2009 and 2014, based on debt figures alone, the south-east African country should have been rated as at medium risk of a debt crisis, but instead this was continually downgraded to low risk.

The debt assessments will continue to be based on how likely a country is to stop paying some of its debts, rather than a broader definition of debt crisis being when debt is preventing the meeting of basic needs or progress towards the Sustainable Development Goals. Furthermore, by applying the current framework to a past database of debt crisis, the IMF and World Bank say the new assessments would still have missed 1-in-5 crises, even based on their own definition of what constitutes a crisis.

Aside from predicting crises, the review presents evidence that past IMF and World Bank assessments have tended to underestimate future debts. It says that 40% of assessments between 2007 and 2010 had large changes (greater than 15% of GDP) on expected debts five years later, and of these, 80% had underestimated what debts would be.

Debts can be a useful form of investment, and global civil society had called for the debt assessments to incentivise the better use of loans by recognising that where good transparency and accountability exist, these means debts are likely to be better spent, and so governments have more space to borrow for useful investments. These suggestions have been largely ignored. However, the IMF’s board, in commenting on the review, said that they would like more action to increase debt transparency, and there are signs that this theme will continue to grow in importance. In the UK, we are campaigning to ensure that all loans to governments under UK law are publicly disclosed when they are given. The UK, alongside New York, are the two jurisdictions under which most loans to governments are made, so the UK government has a key role to play in ensuring transparency is achieved.

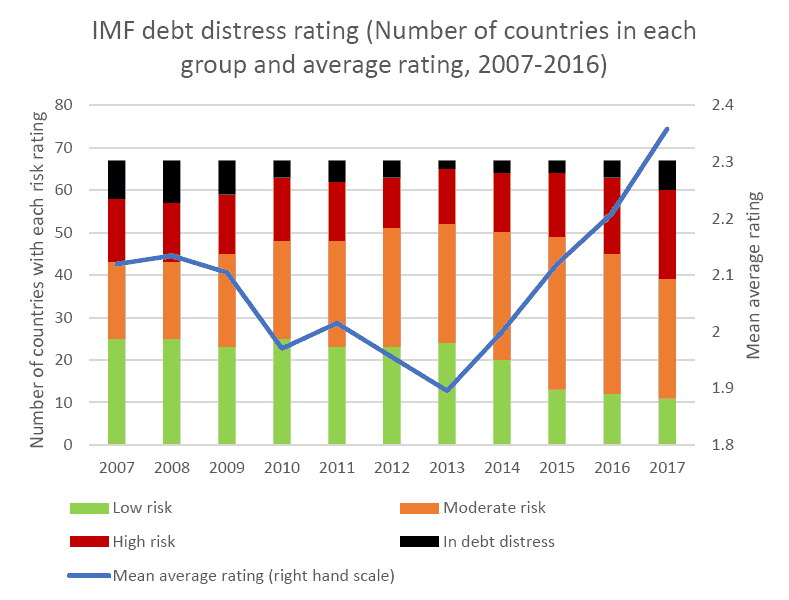

So far this year, three more countries have gone into debt distress on the Fund and Bank’s ratings (Chad, Gambia and South Sudan, joining Grenada, Mozambique, Sudan and Zimbabwe), whilst the number of countries in debt distress or at high risk has increased to 28, from 15 in 2013 (see graph below). Just 11 of 67 countries are assessed as at low risk, the lowest number since assessments began in 2007. The improvements made by the IMF and World Bank to debt assessments, following campaigning by civil society, are unlikely to be enough to prevent a new round of debt crises.