• Government external debt payments reach highest level in the last decade following commodity price falls and rising value of the US dollar

• Figures released before US Federal Reserve meeting where interest rates are expected to be increased again, which will push debt payments higher

Figures released today by the Jubilee Debt Campaign, based on IMF and World Bank databases, show that developing country debt payments increased by 45% between 2014 and 2016 [2]. They are now at the highest level since 2007.

The rapid increase comes after falls in commodity prices in mid-2014 and the rising value of the US dollar. These changes have reduced the income of many governments which are reliant on commodity exports for earnings. They have also caused exchange rates to fall against the US dollar, which increases the relative size of debt payments as external debts tend to be owed in dollars.

Low interest rates in Western countries have also driven a large increase in lending to developing countries in recent years. External loans to low and lower middle income countries have more than quadrupled between 2008 and 2016, from $56 billion to $262 billion.

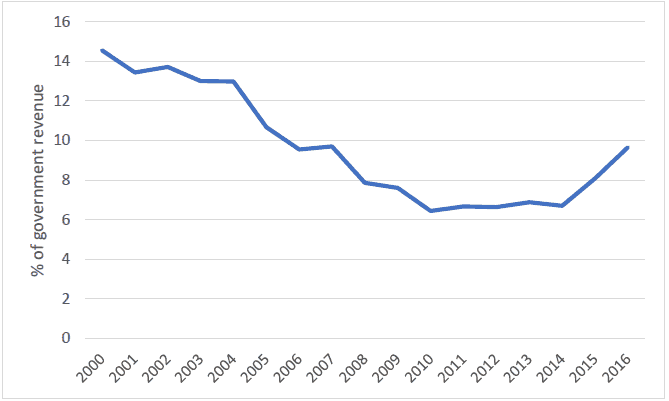

The new figures from Jubilee Debt Campaign show that average government external debt payments across the 122 developing countries for which data is available have increased from 6.7% of government revenue in 2014 to 9.7% of government revenue in 2016, an increase of 45%. This is the highest level since 2007, when such payments were also 9.7% of government revenue (see graph below).

Developing country government average (mean unweighted) external debt payments, as a proportion of government revenue, 2000 – 2016

Tim Jones, economist at the Jubilee Debt Campaign, said:

“The rapid increase in debt payments in many countries comes after a boom in lending, a fall in commodity prices, the rising value of the US dollar and now increasing dollar interest rates. This is putting pressure on government budgets, just when more spending is needed to meet the Sustainable Development Goals.

“In countries where debt crises have arisen, the danger is that IMF and other loans will bail out reckless lenders, increasing debt burdens, and leading to years of economic stagnation, just as in Greece. Instead, reckless lenders should be made to shoulder some of the costs of recent economic shocks by accepting lower payments.”

Countries with the highest debt payments in 2016 include:

• Commodity producers which have been hit by price falls, including Ghana, Mozambique, Angola, Laos and Chad

• Countries on the frontline of refugee flows from Syria – Lebanon and Jordan

• Small states which were previously considered ‘too rich’ to benefit from significant debt relief initiatives, including Grenada, Jamaica and the Dominican Republic.

Mozambique started defaulting on its debt in January 2017. In April 2016, the IMF suspended its loans bailing out Mozambique’s previous lenders, after it was revealed that two London banks, Credit Suisse and VTB Capital, had lent $1.1 billion to two companies in Mozambique, with government guarantees, without the loans being made public, agreed by the Mozambique parliament or disclosed to the IMF.

Developing country external debt payments fell between 2000 and 2010 because of rising prices of commodity exports and the Heavily Indebted Poor Countries Initiative, which cancelled almost $130 billion of debts owed to governments and multilateral institutions for 36 low and lower middle income countries.

The twenty countries with the highest debt payments in 2016 were:

| Country | External debt payments as proportion of government revenue

|

Distinguishing features | Recipient of HIPC debt relief |

| Angola | 44% | Oil producer | No |

| Lebanon | 42% | Hosting large refugee population | No |

| Chad | 39.2% | Oil producer | Yes |

| Ghana | 36.8% | Oil and gold producer | Yes |

| Bhutan | 27.1% | Small state, large debts linked to hydropower | No |

| Montenegro | 26.8% | Recession after 2008 financial crisis | No |

| Sri Lanka | 23.7% | High debt for many years but no meaningful cancellation | No |

| Grenada | 23.5% | Small state, high debt since hurricanes in 2004 and 2005 | No |

| Jamaica | 23.1% | Small state, high debt for many years but no meaningful cancellation | No |

| Gambia | 21.9% | Debt from past dictator | Yes |

| Fiji | 21.5% | Small state | No |

| Belize | 20.9% | Small state, high debt for many years but no meaningful cancellation | No |

| Mozambique | 20.2% | Metals and fossil fuels producer | Yes |

| Malawi | 18.3% | Flood and droughts | Yes |

| Lao PDR | 18.2% | Metals producer | No |

| Jordan | 17.5% | Hosting large refugee population | No |

| Tunisia | 16.6% | Debt from past dictator | No |

| Dominican Rep | 16.3% | Small state, high debt for many years but no meaningful cancellation | No |

| Gabon | 16.1% | Oil producer | No |

| Marshall Islands | 15.1% | Small state | No |

Notes

[1] For more detailed information see our briefing: ‘The new debt crisis in the global South‘ which includes full data tables for all 122 countries

[2] The figure is a mean unweighted average. The median unweighted average has increased by 49% between 2014 and 2016, from 4.9% of government revenue to 7.3%, indicating that this is a general trend rather than due to particular outliers.

Where they are available, the figures for government external debt payments as a proportion of revenue come from IMF and World Bank Debt Sustainability Assessments conducted for individual countries since the start of 2016. In total these cover 44 countries.

For the other 78 countries figures for government external debt payments are from the World Bank’s International Debt Statistics 2017 and figures for government revenue are calculated from the IMF’s World Economic Outlook Database, October 2016

[3] The IMF’s commodity price index fell from 185 in June 2014 to a low of 83 in January 2016. It has since increased to 117 as of January 2017, but this is still 37% below levels in mid-2014.

[4] Bloomberg’s dollar spot index has risen from 80 in June 2014 to 102 as of 8 March 2017, an increase of 27.5%.

[5] For example, since mid-2014, there have been the following falls in currency against the US dollar:

Mozambique metical: down 56%

Malawian kwacha: down 45%

Angolan kwanza: down 41%

Ghanaian cedi: down 36%

Tunisian dinar: down 27%